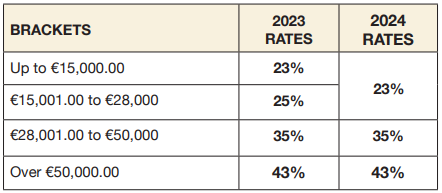

Legislative Decree no. 216/2023 ordered the implementation of the most important personal income tax (IRPEF) reform, providing for a change from 4 to 3 brackets.

For 2024, for the purpose of determining personal income tax, gross tax is calculated as follows:

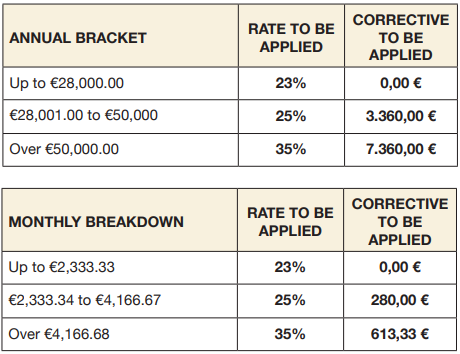

To simplify the calculation of gross tax, the so-called “deduction constants” can be used by multiplying the taxable income by the rate corresponding to the bracket in which the income is included and then subtracting the adjustment for the same bracket.

The following is the reference table:

Examples (based on a year):

- 1. Annual Taxable Income = €29,000.00 • € Gross IRPEF = 29,000.00*35% – 3360 = € 6,790.00.

- 2. Annual Taxable Income = €52,000.00 • € Gross IRPEF = 52,000*43% – 7,360 = € 15,000.00.

Moreover for 2024, the deduction for employment has been raised from €1,880.00 (if total income does not exceed €15 thousand) to €1,955.00.

As a result of the changes, from 2024 onwards there will be a slight decrease in taxes and consequently a slight increase in net income, especially for employees earning between €15,000 and €50,000 per year.

On the other hand, for incomes above €50,000, a correction has been introduced to offset the reduction in the rates for the first brackets, which provides for a reduction in deductions on deductible expenses, except for health expenses, equal to €260. This reduction only has an impact on the filing of one’s tax return.

Finally, for 2024, the “No Tax Area” for employed workers has been equated to that of pensioners. As such, for both types of income, the “No Tax Area” limit will be €8,500.